Blockchain technology has emerged as a game-changer in the modern technological landscape. Initially designed as the underlying technology for cryptocurrencies like Bitcoin, blockchain has grown far beyond its original purpose. It is now being leveraged in a wide array of applications across various industries. In this article, we will explore the role of blockchain in modern technology and its impact on sectors such as finance, supply chain, healthcare, and more.

Understanding Blockchain

At its core, blockchain is a distributed ledger technology that stores data across a network of computers, creating a chain of blocks. Each block contains a set of transactions or data records, and these blocks are linked together in chronological order, forming a chain. The key features of blockchain include:

Decentralization: Blockchain operates on a decentralized network, where no single entity has control. This ensures that no central authority can manipulate the data.

Security: Transactions are secured through cryptography, making it extremely difficult to alter or tamper with the data once it is recorded on the blockchain.

Transparency: All participants in the network have access to the same data, and any changes are visible to all, promoting transparency.

Immutable Records: Once a transaction is added to the blockchain, it cannot be altered or deleted, ensuring the integrity of the data.

Smart Contracts: Smart contracts are self-executing contracts with the terms of the agreement written into code. They automatically execute and enforce contract clauses when predefined conditions are met.

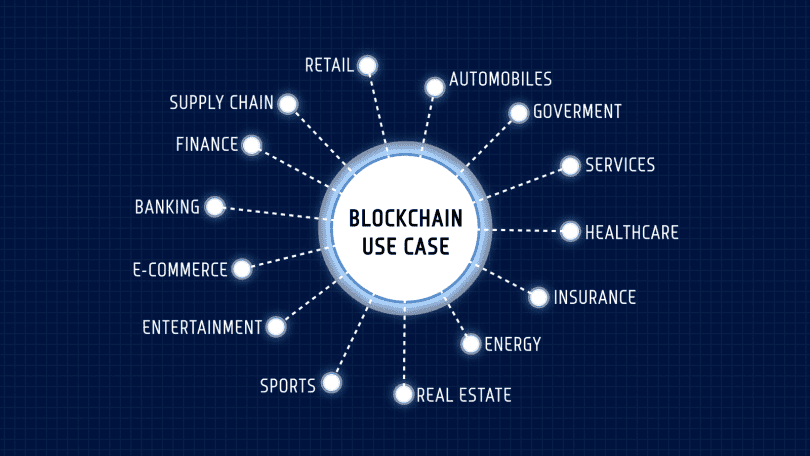

The Role of Blockchain in Various Industries

Blockchain technology has made a significant impact across a range of industries. Here’s how it is influencing modern technology in different sectors:

- Finance and Banking: Revolutionizing Transactions

Blockchain has the potential to revolutionize the financial sector. It enables secure, transparent, and near-instantaneous transactions without the need for intermediaries like banks. Blockchain-based cryptocurrencies, such as Bitcoin and Ethereum, have gained popularity as alternative forms of digital currency. Furthermore, blockchain streamlines cross-border payments, reduces fraud, and minimizes the risk of double-spending.

- Supply Chain Management: Enhancing Transparency

Blockchain brings greater transparency and traceability to supply chain management. Companies can record every step of a product’s journey on the blockchain, from its origin to its final destination. This helps in reducing fraud, ensuring authenticity, and preventing counterfeit goods from entering the supply chain. Additionally, blockchain can streamline logistics and reduce administrative overhead.

- Healthcare: Securing Patient Data

The healthcare industry faces the challenge of securing patient data and ensuring its accuracy. Blockchain can be used to create a secure, immutable ledger of medical records. Patients have more control over their data, and healthcare providers can access accurate and up-to-date information, which can improve patient care. Moreover, blockchain can be used to track the pharmaceutical supply chain, ensuring the authenticity of medications.

- Voting Systems: Ensuring Integrity

Blockchain technology can be used to create secure and tamper-proof voting systems. This would enable transparent and verifiable elections, reducing the risk of fraud and manipulation. Citizens can have confidence that their votes are accurately recorded and counted.

- Intellectual Property: Protecting Creators

Blockchain has the potential to protect intellectual property rights by providing a secure and immutable record of ownership. Artists, musicians, and creators can use blockchain to manage their intellectual property and ensure they receive fair compensation for their work.

- Real Estate: Streamlining Transactions

Real estate transactions involve multiple parties and a complex exchange of assets. Blockchain can simplify and streamline these transactions by providing a secure and transparent ledger of property ownership. This reduces the risk of fraud and errors in property records.

- Energy: Enabling Peer-to-Peer Transactions

Blockchain technology can facilitate peer-to-peer energy transactions in decentralized energy grids. Individuals with excess renewable energy can sell it directly to others in their community, using blockchain to record and verify the transactions.

Challenges and Considerations

While blockchain offers numerous benefits, it also presents challenges and considerations:

Scalability: The current infrastructure of many blockchains faces scalability issues, limiting the number of transactions that can be processed. Solutions such as layer 2 scaling and sharding are being developed to address this challenge.

Regulation: The regulatory landscape for blockchain and cryptocurrencies is still evolving. Governments around the world are working to establish legal frameworks, which can create uncertainty for businesses and investors.

Energy Consumption: Some blockchain networks, especially those that rely on proof-of-work consensus algorithms like Bitcoin, consume significant amounts of energy. This has led to environmental concerns, and there is a push to develop more energy-efficient consensus mechanisms.

Interoperability: As different blockchain platforms emerge, interoperability becomes an issue. Seamless communication and data transfer between various blockchains is a challenge that needs to be addressed.

Privacy: While blockchain offers transparency, it can be at odds with data privacy regulations, such as GDPR. Striking the right balance between transparency and privacy is a complex challenge.

Conclusion

Blockchain technology is playing an increasingly prominent role in modern technology across various industries. Its fundamental features, such as decentralization, security, and transparency, make it a powerful tool for transforming data management and transactions. As blockchain continues to evolve, addressing challenges related to scalability, regulation, and energy consumption will be critical to its widespread adoption.

In the coming years, we can expect blockchain to have an even greater impact, enabling new business models, enhancing security, and creating opportunities for innovation in sectors beyond finance, from supply chain management to healthcare and beyond. As the technology matures, blockchain’s influence on the modern technological landscape is likely to expand, revolutionizing the way we record, transact, and secure data.

+ There are no comments

Add yours